Strait of Hormuz Explained: Why Middle East Tensions Matter for India

SAHI

On June 23, 2025, global oil markets jolted awake.

Brent crude spiked nearly 15% intraday, Indian equities opened sharply lower, and traders scrambled to assess the impact of rising tensions between Iran and the U.S. over a possible blockade of the Strait of Hormuz the world’s most critical oil artery.

But why should a narrow 21-mile channel between Oman and Iran keep Indian traders, policymakers, and retail investors on edge?

Because nearly 40% of India’s crude oil and over 50% of its LNG flow through this single chokepoint. If Hormuz is threatened, it doesn’t just raise prices it raises questions about inflation, currency stability, and portfolio risk.

This blog unpacks the financial implications of the Strait of Hormuz, why it’s back in headlines, and what it means for India’s markets, economy, and energy security.

The Strait of Hormuz may look like a slim stretch of water on the map, but it punches far above its size in geopolitical and financial importance.

What is it?

A narrow passage just 21 miles wide at its tightest point that links the Persian Gulf to the Arabian Sea. On one side sits Iran; on the other, Oman and the UAE. Every day, nearly 20 million barrels of oil pass through it, accounting for 20% of global oil consumption and nearly one-fifth of the world’s LNG trade.

Why does it matter to India?

India sources a large portion of its energy from the Middle East. In fact:

-

About 35–40% of India’s crude oil imports flow through Hormuz

-

Around 42–53% of its LNG comes from Qatar and UAE both reliant on this route

-

Countries like Iraq, Saudi Arabia, Kuwait, and UAE are top suppliers whose tankers must pass through Hormuz before reaching Indian shores

India currently imports 5.5 million barrels per day (bpd) of crude. Of this, around 2 million bpd come via the Strait. That’s not just volume that’s vulnerability.

A single disruption whether due to a military standoff, sanctions, or naval blockade could choke India’s energy lifeline, sending ripple effects through the entire financial system.

The week of June 17–23, 2025 saw tensions escalate rapidly in the Middle East.

Reports emerged of U.S. precision strikes on Iranian nuclear facilities, prompting fiery rhetoric from Tehran. On June 22, Iran’s parliament voted on a resolution authorizing a potential closure of the Strait of Hormuz in response to “Western aggression.” Within hours, global oil markets reacted.

-

Brent Crude surged to a 5-month high, touching $78.89 per barrel

-

Indian benchmark indices opened sharply lower on June 23, with the Sensex dropping 931 points intraday before recovering slightly

-

Nifty closed down 0.56%, while the India VIX shot up, signaling trader anxiety

-

FIIs dumped ₹1,874 crore worth of equities, though DIIs stepped in to stabilize the market

By June 24, the geopolitical storm seemed to ease as global powers called for restraint. Crude prices corrected back to $67.84, and Indian equities stabilized. But for traders, the message was clear: Hormuz headlines move markets fast and hard.

This wasn’t just a regional dispute. It was a reminder that:

-

Oil prices remain hostage to geopolitics, not just supply and demand

-

India’s energy-heavy import structure makes it particularly vulnerable

-

A single chokehold can rattle global markets and your portfolio

If the Strait of Hormuz were fully blocked even for a few days the shock to oil markets could be severe and immediate.

Goldman Sachs warns Brent crude could spike to $110+ per barrel, a nearly 60% jump from current levels.

JP Morgan and other analysts see a 30–40% upside in a moderate disruption scenario.

For India, every $10 increase in crude adds up fast:

-

Import Bill Impact: According to Bank of Baroda, a $10/bbl rise increases India’s oil import bill by over $12 billion annually

-

GDP Drag: Elara Securities estimates this could knock off 0.25–0.3% from GDP growth

-

Inflation Spike: Fuel and transport costs ripple through the economy, potentially raising inflation by 30 basis points or more

-

Trade Deficit Widening: A surge in oil costs could push the trade deficit up by 20–30 bps of GDP, weakening macro fundamentals

And for the Indian retail investor or trader?

It means tighter monetary policy, a weaker rupee, higher fuel prices, and lower profit margins across oil-sensitive sectors like aviation, autos, and logistics.

In essence: Brent above $75 = red alert for India’s fiscal math.

When oil spikes, Indian markets don’t just flinch they tremble.

On June 23, when Brent crude neared $79 amid fears of a Hormuz closure:

-

Sensex fell over 930 points intraday, Nifty briefly slipped below 24,900

-

FIIs pulled out ₹1977 crore in a single session spooked by energy risk and a weaker rupee outlook

-

DIIs stepped in with ₹3,228 crore of buying, cushioning the sell-off

By June 24, as crude eased and global cues improved, markets stabilized. But the underlying fragility was exposed.

Monetary policy is now being shaped not just by domestic factors but by what flows through a 21-mile strait 2,000 km away.

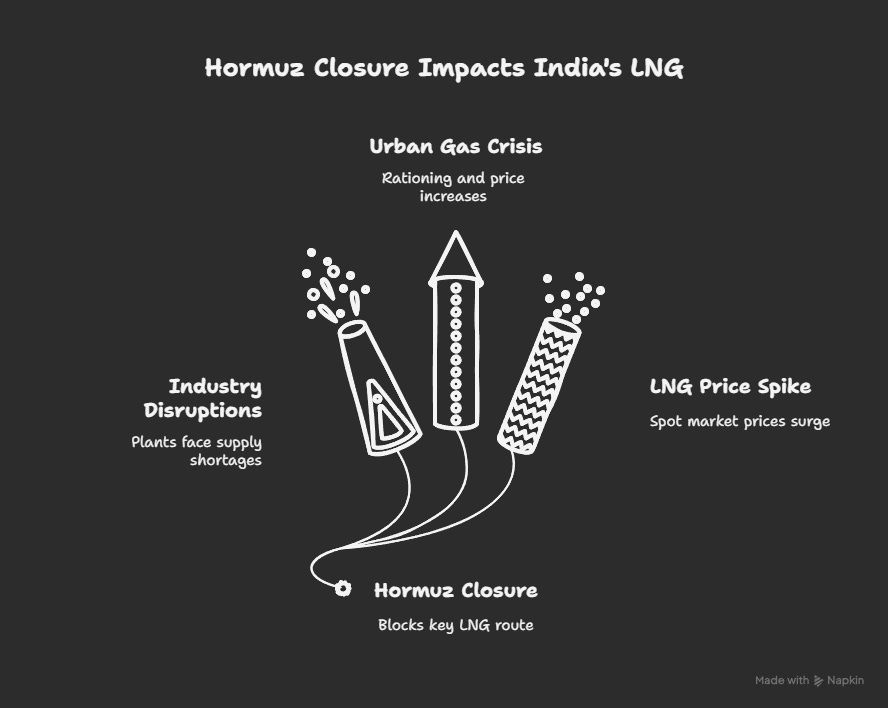

Crude oil gets most of the headlines but LNG is the silent casualty if the Strait of Hormuz shuts down.

India depends on LNG to power industries, feed city gas networks, and keep the lights on in key urban zones. And here’s the catch: over 50% of India’s LNG imports come from Qatar and the UAE both of which rely almost entirely on Hormuz for maritime transit.

-

Industrial Impact: Fertilizer plants, steel mills, and petrochemical units could face supply disruptions or steep input cost inflation

-

Urban Gas Crisis: City gas distribution (CGD) networks may raise prices or ration supply in metros like Delhi, Mumbai, and Ahmedabad

-

LNG Spot Market Spike: LNG spot prices could surge overnight, disrupting long-term contracts and supply planning

Yes but only partially.

Indian refiners and OMCs maintain strategic reserves covering 9–15 days of crude and several weeks of commercial LNG inventory. But that’s short-term armor, not long-term insulation.

If the Strait remains blocked for even 3–4 weeks, India would be forced to:

-

Reroute tankers via Cape of Good Hope or Suez Canal, raising freight and insurance costs

-

Tap into strategic petroleum reserves, which cover about 9–10 days of full consumption

-

Accelerate purchases from non-Gulf suppliers which may not be able to fill the gap instantly

India knows it cannot afford to be held hostage by the Strait of Hormuz. Over the past few years, it has quietly but deliberately rewritten its energy playbook diversifying supply chains, building financial buffers, and reworking diplomatic channels.

Ten years ago, over 60% of India’s crude came from West Asia. Today, that figure has dropped sharply:

-

Russia now accounts for over 40% of India’s crude a jump from just 2% in 2021

-

Alternative routes via the Suez Canal, Cape of Good Hope, and Atlantic lanes bypass Hormuz entirely

-

Contracts with West Africa, the U.S., Brazil, and Latin America have become core to Indian refiners

This diversification was tested on June 23 and it worked. Indian refineries leaned on non-Gulf suppliers to maintain steady crude inflow even as prices spiked.

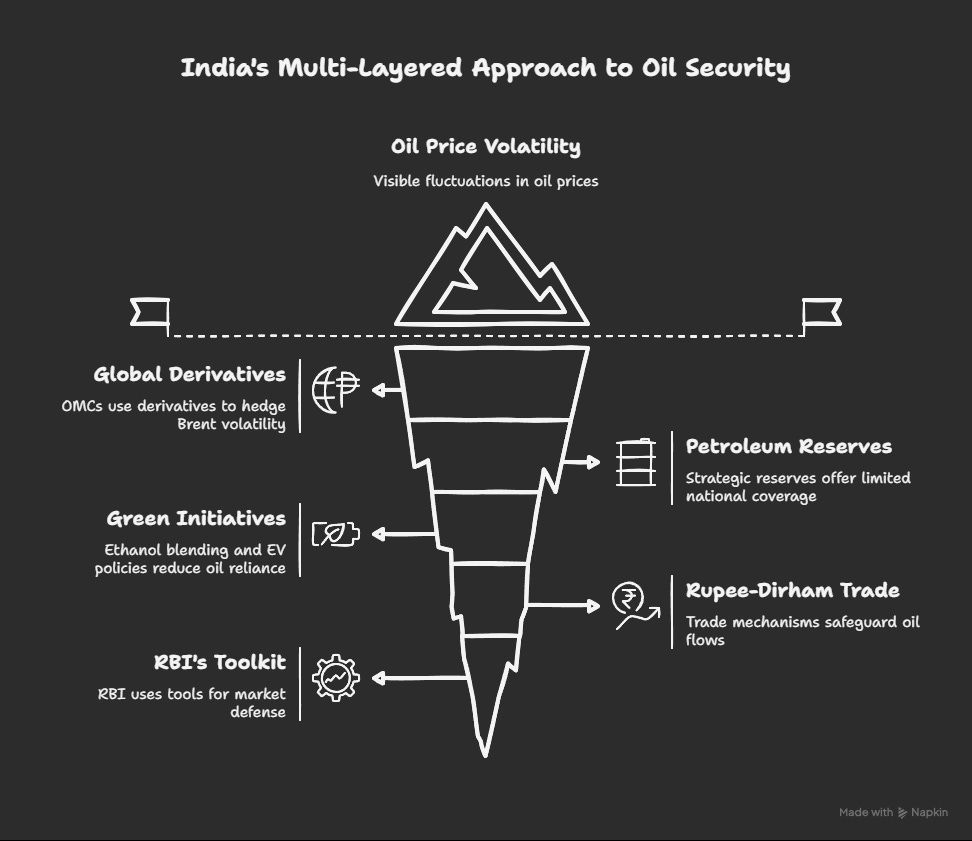

India isn’t just shifting tankers it’s building insulation:

-

OMCs hedge Brent volatility using global derivatives

-

Strategic petroleum reserves hold ~39 million barrels offering 9–10 days of national coverage

-

Green push: ethanol blending, EV policies, solar incentives slowly reduce oil reliance

-

Rupee-dirham trade mechanisms with the UAE safeguard oil flows even if dollar liquidity dries up

-

RBI’s toolkit rate cuts, forex intervention, liquidity support remains India’s first line of market defense

Short answer: less vulnerable, not immune.

-

40% of India’s oil and 50% of its LNG still pass through Hormuz

-

A brief disruption spikes freight and insurance costs; a prolonged one could test SPRs, currency buffers, and investor nerves

-

FIIs watch oil and rupee trends closely every spike chips away at macro confidence and narrows monetary flexibility

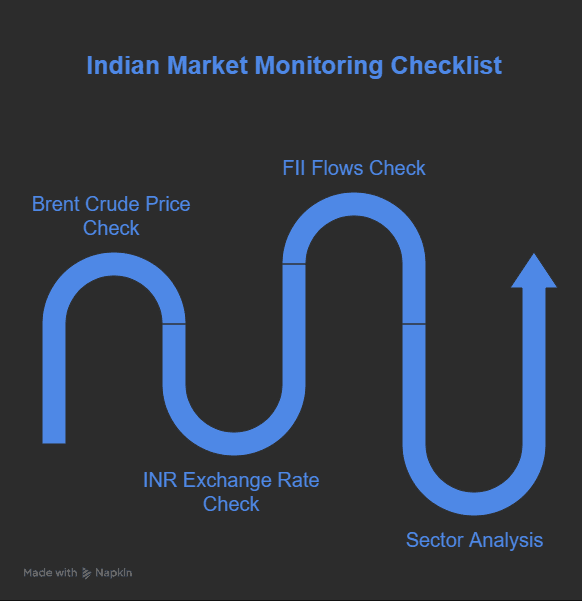

In times of Hormuz stress, macro > micro. Here’s your checklist:

-

Brent Crude > $75? Inflation alert. Bond yields could rise, equities may wobble

-

INR near 87/$? RBI may step in expect forex market volatility

-

FII flows turn negative? Sentiment shift. Time to reassess positions

-

Watch sectors:

-

Negative: Airlines, logistics, paint, FMCG (fuel-intensive)

-

Volatile: OMCs, gas utilities, city gas

-

Tailwinds: Ethanol, solar, green energy plays

-

The Strait of Hormuz is calm today, but its threat is ever-present. Even one blockade or misfire can ripple through your P&L. India’s response from sourcing strategy to financial defense is robust but not foolproof.

Stay informed. Stay hedged. And always respect the geopolitical undercurrents that drive financial markets.